Mortgage

The right home loan will give you the go-ahead to make more memories.

With so many home loan products available to homebuyers, it can sometimes be hard to determine which one is the right one for you. Whether considering a government-backed mortgage product or a conventional loan, there are many factors to weigh, from interest rates to repayment schedules.

In this blog we’ll answer your basic questions about conventional loans, compare fixed- and adjustable-rate mortgages, and offer simple advice for how to choose the best loan for your needs. Keep reading to learn more!

Conventional mortgages are loans provided by a private bank, lender, mortgage company, or other financial institution—and not guaranteed by the federal government. They can come with a fixed interest rate that stays the same for the life of your loan, or a rate that adjusts over time—we’ll take a closer look at these differences below. Conventional loans can also be conforming or non-conforming.

What is a conforming loan? A conforming loan is a conventional loan that is for or below $762,200 and that meets (or “conforms”) to certain requirements for approval. The Federal Housing Finance Agency (FHFA) sets the loan limit dollar amount for conforming loans. Other qualifying criteria for conforming loans are set by the Federal National Mortgage Association (commonly known as “Fannie Mae”) and the Federal Home Loan Mortgage Corporation (commonly known as “Freddie Mac”)—government sponsored organizations that invest in mortgage loans.

So, what is a non-conforming loan, then? Non-conforming loans are simply loans that don’t “conform” to these standard limits and criteria for approval. These include conventional loans for larger amounts (sometimes called “jumbo loans”), as well as government-backed loans with different qualification requirements (like VA, USDA, and FHA loans).

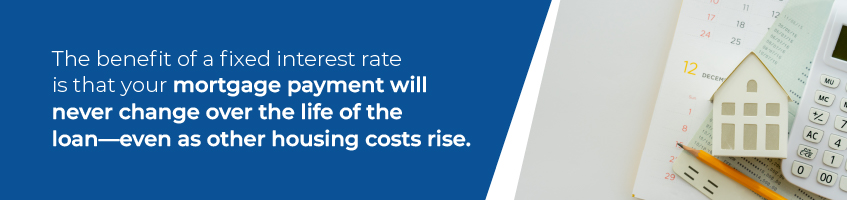

Most home loans—conventional or not—are fixed-rate mortgages. These loans have a fixed interest rate for the entirety of the loan, avoiding interest changes based on market fluctuations. The benefit of a fixed interest rate is that your mortgage payment will never change over the life of the loan—even as other housing costs rise. This can mean your home loan becomes more affordable over time with regular inflation or as your income increases. However, it’s important to note that your property taxes and insurance costs may go up, so your monthly escrow payment may still increase, even if your loan payment (principal and interest) does not.

The most popular term length for fixed-rate mortgages is 30 years, but you can also apply for a 10-, 15-, or 20-year mortgage. Use BTC Bank’s Fixed-Rate Mortgage Loan Calculator to see how much interest you could realistically pay with a fixed-rate mortgage, based on your term length and expected interest rate.

Adjustable-rate mortgages are a little more complicated. They start off similarly to a fixed-mortgage. For the initial repayment period of your loan, the interest rate will remain the same. Once the introductory period is over, the rate will vary from year to year depending on market index rates. When interest rates tend to be higher, you can expect your rate to follow suit. When they go down, your rate may as well.

So how long is this introductory period of fixed interest? That depends on the type of ARM you have. 5/1 ARMs (the most common form of ARM) have a 5 year fixed-rate period, followed by annual (every 1 year) interest changes. Other popular ARM configurations include 3/1, 7/1, and 10/1.

The benefit of ARMs is that the initial interest rate is often lower than the market rate you may pay with a fixed-rate mortgage. Often, people choose an ARM because they plan to sell their house within that initial period. Alternatively, individuals may choose to refinance with a fixed rate mortgage after the initial fixed period ends—especially if they expect their rate to rise.

However, when market rates are high, an ARM can not only provide you with a lower initial rate, it can prevent you from locking in a high interest rate for a long loan term. Remember, after the initial period, your rate will be based on prevailing market rates. If interest rates come down significantly, yours may as well.

Use BTC Bank’s ARM Calculator to determine what your payments might be.

Which home loan will work best for your needs and make the most financial sense for you depends on a number of factors including current interest rates, how long you plan on staying in your home, and your current financial situation (compared to where you plan to be in the future).

A fixed-rate mortgage may make sense if:

An adjustable-rate mortgage may make sense if:

A note on interest: To reign in inflation, the Fed often raises their interest rates on overnight deposits in Federal Reserve Banks to encourage banks to also raise interest rates for their loans. During times of high inflation, mortgage rates tend to be higher because of this practice. Knowing the relationship between inflation and interest may help you predict whether or not to expect interest rates to rise or fall in the future.

When comparing mortgage products and weighing interest costs, remember to take advantage of our 10, 15, or 30-Year Fixed-Rate Mortgage Loan Calculator and Adjustable-Rate Mortgage Loan Calculator.

If you have a government-backed mortgage like an FHA loan, it is possible to refinance to a conventional mortgage with BTC Bank. You may choose to do this to eliminate your mortgage insurance premium or other fees, get a better interest rate (especially if your credit has improved since your original loan), or use the equity in your home for other purposes like consolidating debt or renovating your home (also known as a “cash-out refinance”).

Both adjustable- and fixed-rate mortgages require a minimum of a 5% down payment and a credit score of 620, depending on your financial situation. If you are able to meet these requirements, you may qualify to refinance your mortgage with a conventional Adjustable-Rate Mortgage or Fixed Rate Mortgage with BTC. Speaking to an experienced lender can help you determine if refinancing makes sense for you.